The commencement of the new financial year highlights the importance of preparing for upcoming lodgement deadlines.

To assist you, we have outlined key dates for various obligations to your employees and the ATO for the next year. *This list is not comprehensive, and additional lodgements may be necessary depending on your specific circumstances or industry.

SINGLE TOUCH PAYROLL (STP)

For Unrelated Employees

Employers must lodge STP finalisation declarations with the ATO by 14 July each year for all arm’s length or unrelated employees.

For Mixed Employee Groups

If your workforce includes both closely held and unrelated employees, the deadline for lodging your STP finalisation event is extended to 30 September.

For Closely Held Employees Only

For employers with only closely held employees, the STP finalisation is due when the individual tax returns of those employees are due.

Accessing Income Statements

Once the STP finalisation declaration is lodged, employees can access their income statements through the ATO online services linked to myGov.

Not Using STP?

If you are not yet using STP, you must provide all employees with a payment summary by 14 July.

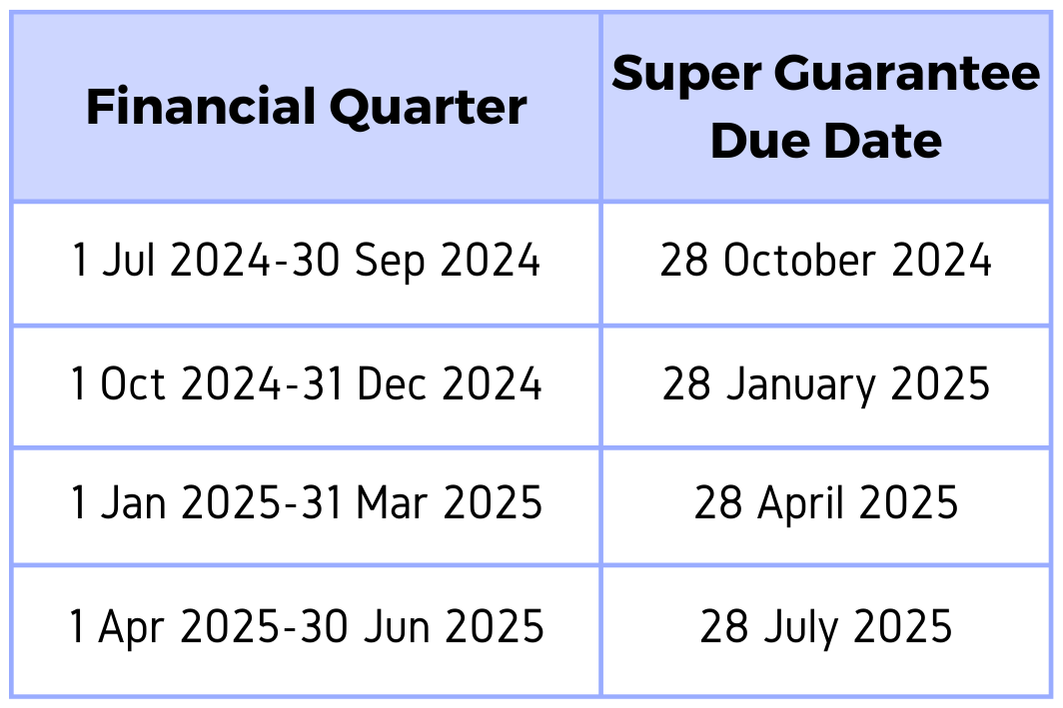

SUPER GUARANTEE (SG)

Employers are required to pay the minimum superannuation guarantee (SG) on time to avoid incurring the Super Guarantee charge. This obligation begins from the day your employees start working. Effective 1 July 2024, the SG rate will be 11.5% of wages paid to eligible employees. SG payments are due quarterly, 28 days after the end of the previous financial quarter. Please refer to the table below for the specific payment due dates.

Payment Due Dates on Weekends or Public Holidays

If an SG payment due date falls on a weekend or public holiday, your contribution must be received by the super funds on or before the next business day.

Frequency of Payments

You can make SG payments more frequently than quarterly (e.g., fortnightly or monthly). However, ensure that the total Super Guarantee contribution for the quarter is paid by the due date.

Late or Missed Payments

If you miss or make late super payments, you will need to pay the superannuation guarantee charge (SGC), which is not tax-deductible.

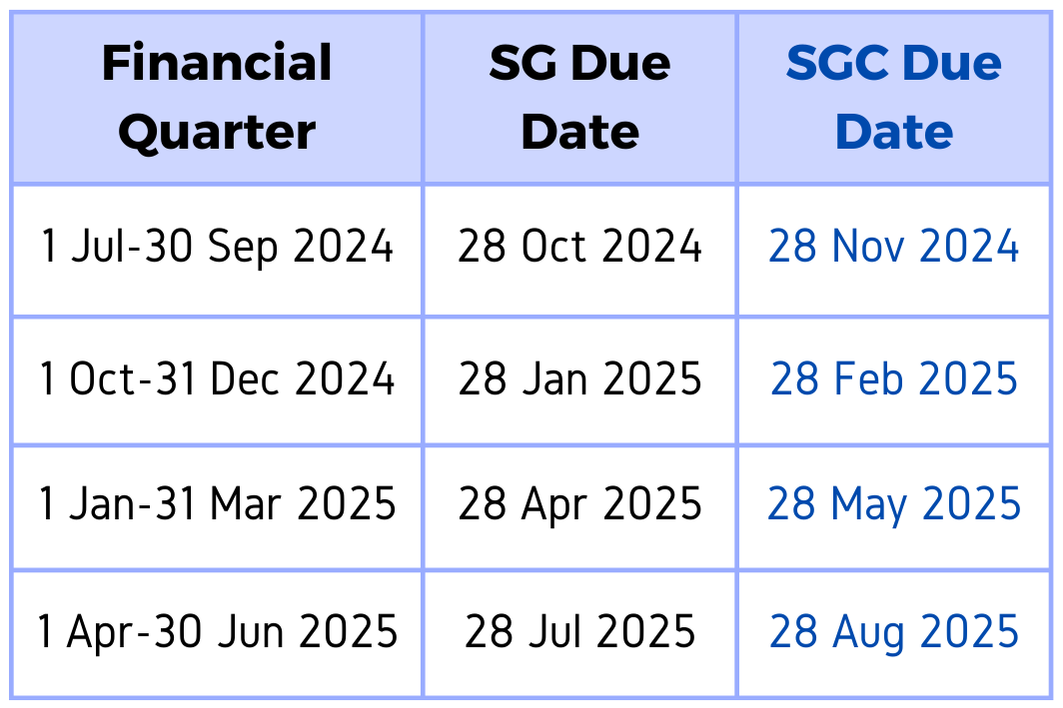

SUPER GUARANTEE CHARGE STATEMENT (SGC)

Employers are liable for the additional SGC when the super guarantee is not paid by the due date. This charge, along with the associated SGC statement, is due to the ATO within one calendar month after the SG due date. Please refer to the table below for the specific payment and lodgement due dates.

Failure to provide an SGC statement when required, by lodging your SGC statement late, or failing to provide a statement or information when requested during an audit, could result in the maximum penalty of 200% of the SGC.

ACTIVITY STATEMENTS

Monthly Lodgements

Businesses with an annual GST turnover of at least $20 million are required to report and pay GST monthly by lodging a business activity statement (BAS) through ATO online services for businesses.

PAYG Reporting

If you are an employer with pay as you go (PAYG) withholding amounts between $25,001 and $1 million per year, you must also report and pay your employees’ tax withholding amounts monthly via an instalment activity statement (IAS).

Due Dates

The due date for submitting your monthly BAS or IAS is the 21st day of the month following the end of the taxable period. Please refer to the table below for specific payment and lodgement due dates.

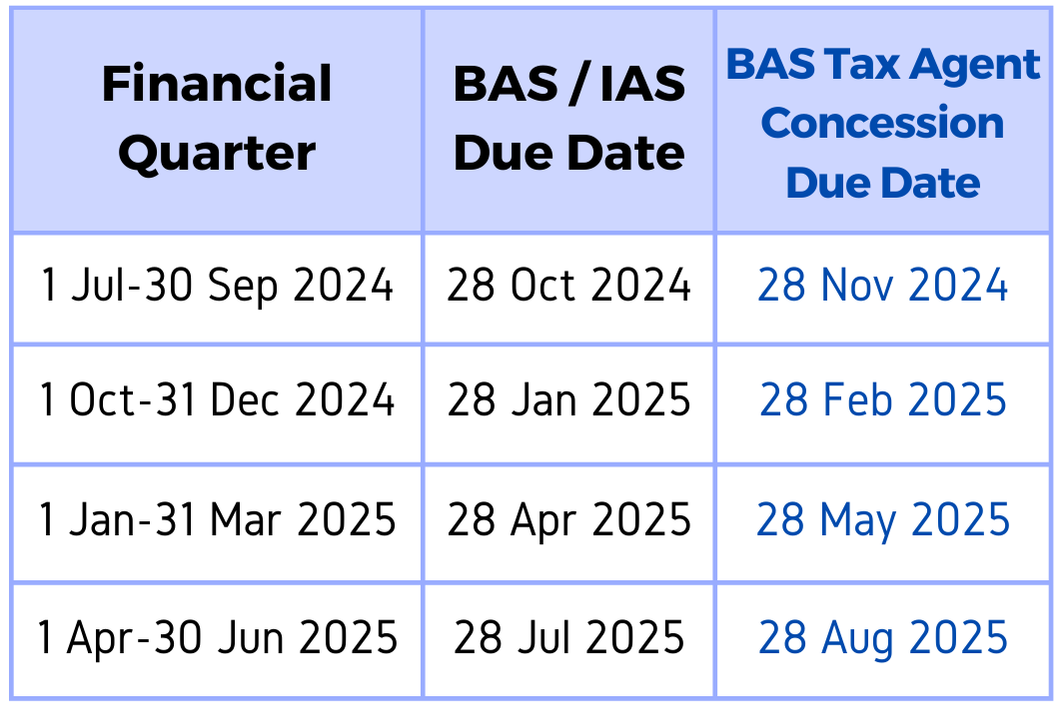

Quarterly Lodgements

BAS

Businesses with an annual GST turnover of less than $20 million are required to lodge a business activity statement (BAS) to report and pay GST quarterly.

PAYG Reporting

Employers with PAYG withholding amounts below $25,000 per year must report and pay the associated tax quarterly via an instalment activity statement (IAS).

Due Dates

A quarterly BAS or IAS is due for lodgement and payment on the 28th day of the month following the end of the quarter. Businesses that lodge their activity statements through a tax agent may benefit from a concessional due date, which is approximately one month after the original due date. Please refer to the table below for specific payment and lodgement due dates.

TAXABLE PAYMENTS ANNUAL REPORT

Businesses operating in the building and construction, cleaning, courier services, information technology, and security industries are required to submit a Taxable Payments Annual Report (TPAR). The TPAR must detail payments made to contractors during the previous financial year and is due for lodgement with the ATO by 28 August each year.

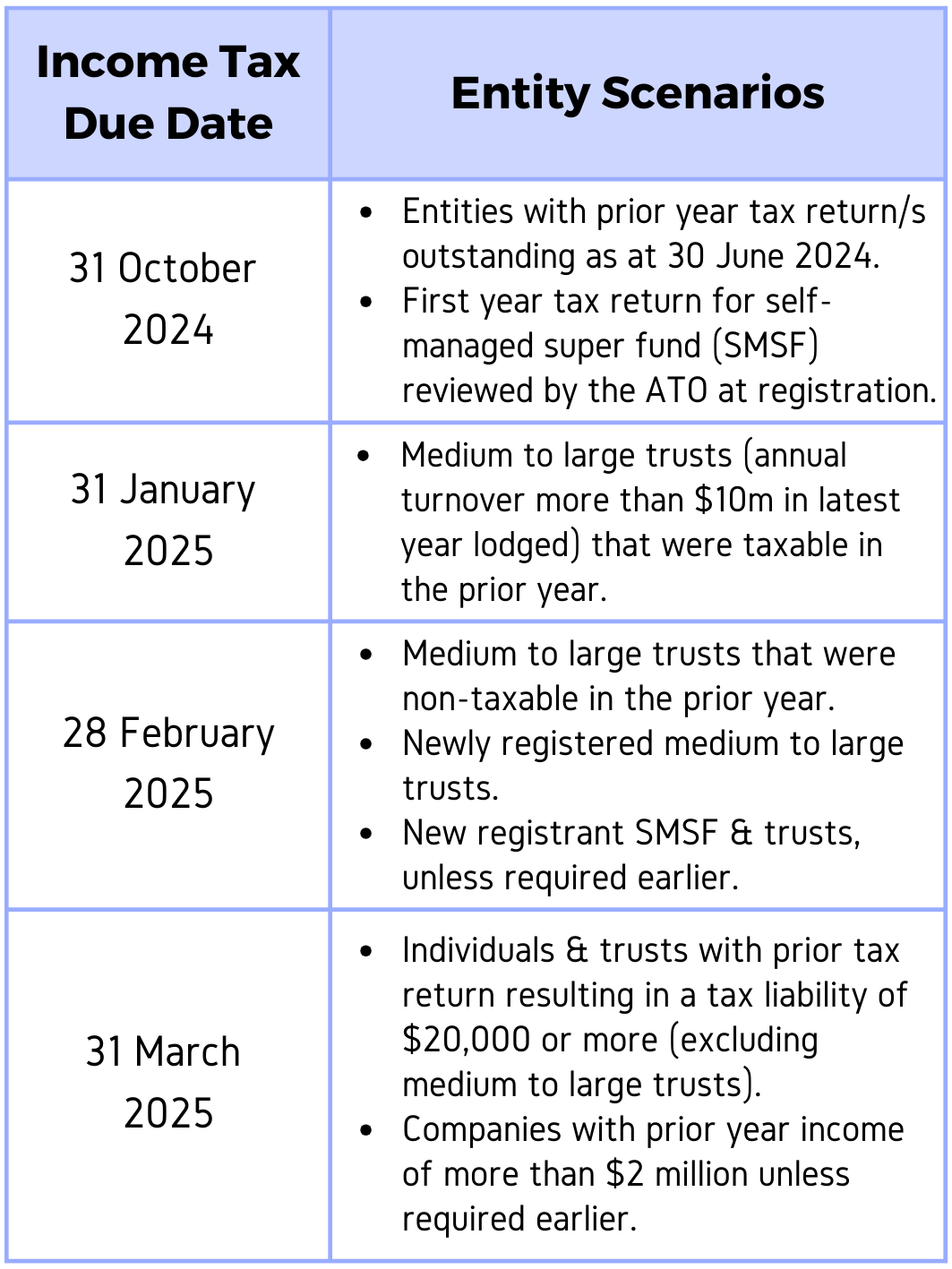

INCOME TAX

Tax Agent Lodgement

If you engage a tax agent to prepare your tax returns, you will generally have until 15 May to lodge and pay any associated income tax for the previous financial year ended 30 June.

Early Lodgement Requirements

In certain circumstances, some entities may need to lodge their income tax returns earlier than the standard due date. Please refer to the due dates below.

TIPS TO MEET YOUR DEADLINES

Here are some practical tips to help you stay on top of your obligations:

-

-

- Set Recurring Events: Create a recurring event or task for each obligation in your digital calendar.

- Set Reminders: Schedule a reminder for a week before the due date to give yourself ample time to address any outstanding matters.

- Add Due Dates: Dedicate time to mark all relevant due dates in a physical calendar that you frequently check.

- Seek Assistance: If you’re unsure about any due dates, reach out to us. We can review your situation and provide clarity.

- Ask for your bookkeeper’s help: If you have a bookkeeper, ask if they can assist with obligations such as lodging Activity Statements. Ask your bookkeeper to remind you when your lodgements are approaching

-

NEED SUPPORT?

We take pride in our ability to alleviate stress and ensure you stay on track, allowing you to focus on what truly matters – the success of your business. Don’t hesitate to contact us via email, or call us on (02) 4455-5333 – we’re here to help manage any outstanding obligations and offer expert advice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}